KAMPALA —The communications sector in Uganda continues to demonstrate resilience as it weathers the storm driven by COVID19, with the latest market performance report showing modest growth across several indicators.

According to the quarterly market tracking report produced by Uganda Communications Commission (UCC), there was a net account addition of 590,000 mobile and fixed subscriptions in the period January to March 2021. This resulted in the overall growth of Total Revenue Earning Customers (REC) from 27.7 million in December 2020 to 28.3 million accounts at the end of March 2021.

Despite this growth marking the first time that total subscriptions have crossed the 28 million mark since the pre-COVID19 peak of March 2020, it also represents a 2% quarter-on-quarter growth, the lowest rate of growth recorded in the last two quarters. Nevertheless, this modest recovery in subscriptions puts Uganda at a phone penetration of almost Seven lines for every 10 individuals in the country.

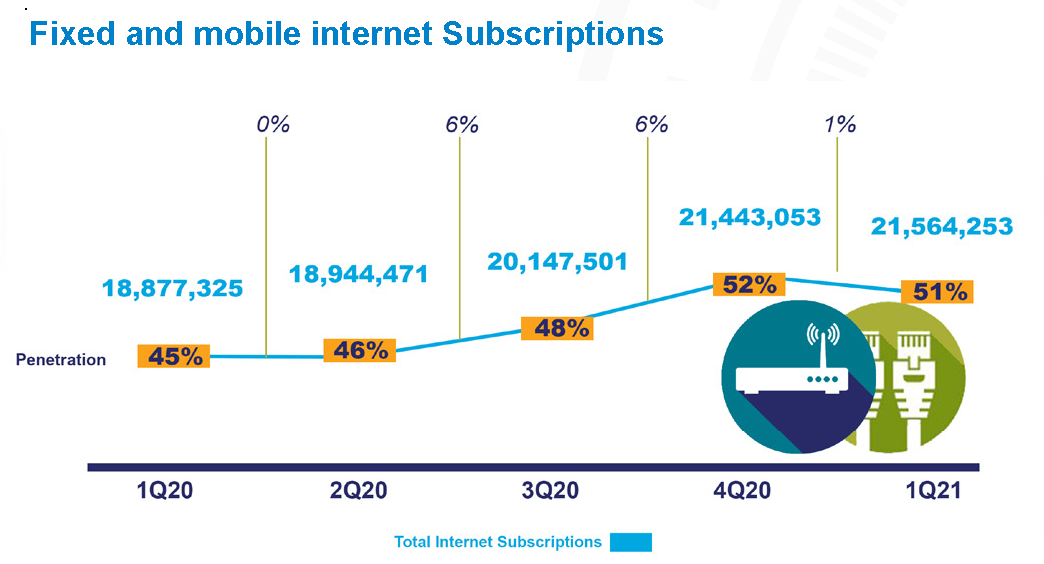

On the other hand, broadband cellular subscriptions stood at 21.5 million in March 2021, including a net addition of 120,000 new subscriptions. While the quarterly net additions have not matched the more than 1 million subscriptions posted in the last quarter of 2020, this is still noteworthy growth given the internet and social media restrictions during the period, as well as the traditional network churns, which usually follow the end of year holidays.

In the mobile network space, the highlight of the quarter was the award of the third National Telecom Operator license to Tangerine Ltd, trading as LycaMobile Uganda, on 24th March 2021. The provisional license permits LycaMobile to deploy national telecommunications infrastructure and provide licensed telecommunications services across all the regional license zones defined by the licensor.

Responding to concerns about expiring data, MTN Uganda became the first provider to launch non-expiring bundles under its flagship 4G Freedom at the end of the first quarter of 2021. This set the tone for an industry-wide review of bundle validity terms, as Smile Telecom introduced its Data King Bundle of 115 GBs while LycaMobile maintained its flagship 100 GB and 50 GB bundles.

Meanwhile, mobile financial services continued to grow, especially in Africa, propelled in part by travel restrictions and other COVID19 fighting measures. At the end of March 2021, total mobile money accounts on the continent had grown to 562 million, translating into a penetration of 40 lines per 100 inhabitants.

The total number of active accounts had grown to 160 million, translating into an account activity ratio of almost 30%, with Vodafone, MTN and Airtel jointly accounting for more than 50% of this account base. The growth in the mobile money business has been so significant that by March 2021 MTN, Airtel and Vodafone mobile money outfits were valued at almost USD 20 billion.

To streamline this growing service in Uganda, the telecom giants MTN and Airtel were issued with a no objection to separate their digital finance business (mobile money) from the cellular network operations. “These no objections are in partial fulfilment of new regulatory obligations instituted by the National Payments Systems Act 2020 and the Uganda Communications Pricing and Accounting Regulations 2019,” the report stated.

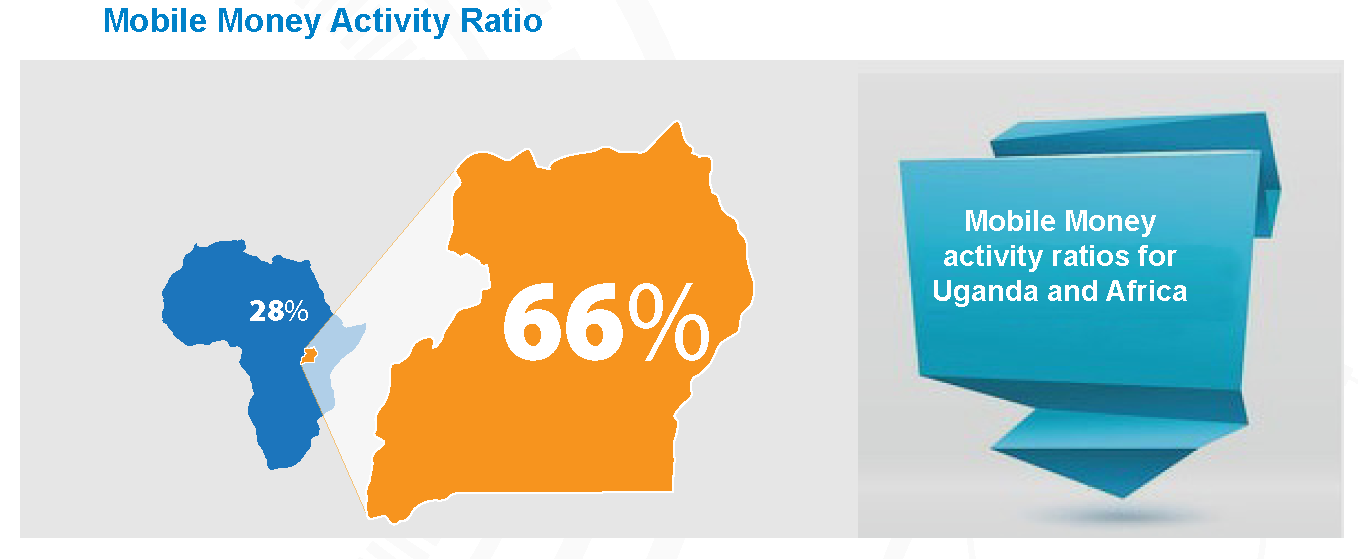

Still on mobile money, following a clean-up of mobile network operators’ account registers, the number of active mobile money accounts was revised downwards, from 22.5 million to 20.3 million at the end of March 2021. This represents 66% of the 30.5 million registered mobile money accounts. The 66% active accounts amounts to double the African average of 30% account activity. On a year-on-year comparison, more than 5 million new accounts were registered between March 2020 and March 2021. This growth was largely fuelled by significant fee waivers, increased merchant acceptance and limited movements at the height of the pandemic.

As a whole, the telecommunications industry yet again posted quarterly gross revenues over and above the 1 trillion mark, with UGX 1.12 trillion recorded between January and March 2021. This reflects a 7% increase in gross revenue compared to the first quarter of 2020 when revenues stood at UGX 1.05 trillion. In terms of quarter-on-quarter comparison, industry revenues dropped by UGX 20 billion from the previous record quarterly performance of UGX 1.14 trillion in December 2020 to UGX 1.12 trillion in March 2021.

On the global scene, with remote working and social distancing continuing to define the “new normal”, the period under review saw increased digitisation and use of social media. Facebook reported an active account base of 2.74 billion users, closely followed by 2.3 billion YouTube accounts. It could therefore be implied that nearly 4 out of every 10 persons globally have a social media account.

As for peer-to-peer messaging applications, WhatsApp posted 2 billion active users while Asian chat powerhouse WeChat/Weixin reported an estimated 1.2 billion active users at the end of March 2021.

On the other hand, image and video sharing applications such as TikTok, Instagram and Snap Chat reported a combined user base of 2.4 billion accounts at the end of the same period. The quarter also witnessed growing subscriptions for new kid on the block Clubhouse, an audio chat social media application launched at the peak of COVID19 lockdowns. Clubhouse’s active accounts had grown to more than 2 million by the end of March 2021.

Meanwhile, Zoom and Microsoft Teams (MS) Teams continued to dominate the remote working market, accounting for 445 million active accounts. In terms of users, Microsoft Teams posted 145 million daily active users in 1Q21 compared to Zoom’s estimated 300 million.

FULL REPORT – MARKET PERFORMANCE REPORT FOR Q1 2021

Continued Rise of Social Media Applications

1Q21 saw increased digitisation and dependence on online messaging channels as social distancing, and remote work remained deeply ingrained in the workplace and social relationships. What came to be known as a COVID third wave continued throughout Europe and the Americas.

At the end of March 2021, Social media giants continued posting record new accounts during the period.

Facebook reported an active account base of 2.74 Billion users, closely followed by 2.3 Billion YouTube accounts. Therefore, it can be implied that almost 4 out of every ten persons globally have a social media account. Thus, social media indeed continues to have an inescapable presence in our everyday lives.

In the world of Peer to Peer messaging applications, WhatsApp Messenger posted 2 Billion active users. In comparison, Asian chat powerhouse WeChat/Weixin reported an estimated 1.2 Billion active users at the end of March 2021.

On the other hand, image and video sharing applications such as TikTok, Instagram and Snap Chat reported a combined user base of 2.4 billion accounts at the end of the review period.

Audio-based online chat forums

Relatedly, there was continued growth in subscriptions for Clubhouse, an audio chat social media application launched at the peak of the global Corona lockdowns. This is similar to live audio debates and political talk shows of the Mid 2000s, popularly known as “Bimeeza” but with a much bigger global audience and reach.

Clubhouse active accounts have grown to more than 2 million at the end of March 2021. Part of this growth has been fuelled by celebrity endorsements and appearances like Tesla CEO Elon Musk’s appearance on The Good Times Show and Robin Hood CEO Vlad Tenev’s discussion on GameStop Shares on Clubhouse. In addition, celebrities like Oprah Winfrey, Drake and Kevin Hart maintain an active presence on the platform.

Business Communication and Remote Working Applications

Zoom and Microsoft Teams (MS) Teams dominate the remote working market accounting for 445 million active accounts. In terms of users, Microsoft Teams posted 145 million daily active users in 1Q21 compared to Zoom’s estimated 300 million.

So prevalent have Zoom and Teams meeting and conferencing applications grown to become the go-to learning platforms even at elementary schools in the global south.

Online Privacy vulnerabilities

The increased dependency on Over-the-Top Applications and other social media applications has not come without challenges as more people get online. For example, at the beginning of the quarter, personal data for more than 500 million Facebook accounts were compromised and leaked online by a group of hackers.

More than 32 million leaked accounts were apparently for users from the USA, while the rest were distributed across more than 100 countries.

Allegedly, Clubhouse and LinkedIn applications also faced data scraping breaches from third-party applications.

Consent Solicitation for third party data sharing

Whatsapp – Facebook Data Share Consent

At the beginning of 1Q21, P2P messaging application WhatsApp notified its more than 2 Billion users that it would be sharing some of its customer data, essentially profile identifiers like mobile numbers, with its parent company Facebook.

This accept or leave terms update was to take effect on 8th February 2021 but was pushed to 2Q21 following widespread complaints from consumers and privacy advocates.

The move has also seen double-digit monthly growth in downloads of other peers to peer messaging applications like Signal and Telegram, apparently on strong privacy ethos.

Apple

In a strategic shift from Whatsapp and Facebook, towards the end of 1Q21 global software and hardware giant, Apple announced its intent to solicit active consent from its customers to share their data to third-party This is a significant shift from current practise where data sharing consent is assumed until one actively opts out.

This fundamental change has not gone without objection from major OTT providers who have in part argued that the new restrictions are a move by OS and Hardware vendors to exclude them from some consumers anticompetitively. Further, they argued that it is not that the applications are collecting any more data than they have previously been collecting.

Global handset shipments

Global handset shipments continued to grow, with market analysts projecting a 7.7% year on year growth in smartphone shipments during 1Q21.

5G is expected to be the most significant growth driver for developed markets, whereas the strong demand for 4G phones following the pandemic will drive demand in emerging markets.

Growth in Mobile Financial Services

The enhanced travel restrictions have seen unprecedented adoption and penetration of mobile financial services. For example, on the African continent, At the end of 1Q21, total mobile money accounts on the continent had grown to 562 Million, translating into 40 lines per 100 inhabitants.

In terms of active accounts, the total number of active accounts had grown to 160 million translating into an account activity ratio of almost 30%.of the 160 Million accounts, Vodafone, MTN, and Airtel accounted for more than 50% of this account base.

So significant has been the growth in MNO mobile money businesses that at the end of 1Q21, the MTN, Airtel and Vodafone mobile money outfits were valued at almost 20 Billion dollars.

Multimedia and the Scientific Election Season

Restricted movements and Social Distancing protocols occasioned by the pandemic mandated that the 2021 national and local council elections (in 1Q21) essentially played out on electronic communications platforms.

For the first time in Uganda electoral history, electronic media channels outpaced traditional mass rallies and the use of print campaign material.

The shift in campaign strategies provided a welcome boost to small regional media outlets and created a new breed of social media political strategists and influencers.

In January 2021, most broadcasters (TV and Radio) registered bookings and sponsorships for more than 95% of primetime broadcast slots by candidates and their agents.

On the digital front, Presidential candidates garnered tens of thousands of followers in the short campaign season. So rapid was the media presence of presidential candidates that most of them got “verified” by various social media platforms at the end of the campaign season.

The season also brought the first use of live online broadcasts as different political actors reached out to the electorate over social media channels.

Traditional Print Media Goes Digital

In print media, January 2021 may turn out to be a landmark point in the distribution of the traditional print Dailies in Uganda. At the beginning of 1Q21, the print giants New Vision and Daily Monitor launched paid online e-paper versions of their dailies in Uganda.

3rd National Telecom Operator License Award

In the mobile network space, the highlight of 1Q21 was the award of the third National Telecom Operator license to Tangerine Ltd T/A LycaMobile Uganda on 24th March 2021. The provisional license permits the licensee to deploy national telecommunications infrastructure and provide licensed telecommunications services across all the regional license zones defined by the licensor.

In its application to the Commission, Lycamobile pledged to roll out at least 550 radio sites across the country within 12 months of license award. This pledge is in pursuit of the 90% geographical coverage obligation established in the license. Accordingly, LycaMobile shall continue using the 0726100000 and 0726999,999 number ranges.

Separation of Airtel and MTN Mobile Money Units

During 1Q21, Airtel Mobile Commerce Ltd, the subsidiary of Airtel Africa Group and Airtel Uganda Limited, the licensed NTO, were issued with no objection to separate Digital Financial Services (DFS) from Airtel’s Cellular Network Operations.

Relatedly, MTN Mobile Money Uganda Limited, part of the MTN Group, was issued with no objection to separating MTN Digital Finance and Cellular Operations.

These no objections partially fulfil new regulatory obligations instituted by the National Payments Systems Act 2020 and the Uganda Communications Pricing and Accounting Regulations 2019.

Under the new dispensation, the mobile money and the cellular operations unit will file access agreements between the two entities for the Commission’s appraisal of potential consumer and competition challenges posed by the partnership. This is in line with the UCC’s Access and Interconnect regulations of 2019

Telephone Subscriptions

The industry posted a net account addition of 590,000 mobile and fixed subscriptions. Total Revenue Earning Customers (REC) grew from 27.7 million in December 2020 to 28.3 million accounts at the end of March 2021.

This is the first time that total accounts have crossed the 28 million mark since the pre-Covid peak of March 2020. However, this growth in subscriptions realised in January to March 2021 resulted in a 2% quarter-on-growth, which is the lowest growth recorded in the last two quarters.

The recovery in subscriptions resulted in penetration of almost seven lines for every 10 individuals in Uganda.

Broadband subscriptions

As of March 2021, broadband cellular subscriptions stand at 21.5 million, with an observed net addition of 120,000 new subscriptions.

While the quarterly net additions have not matched the more than 1 million subscriptions posted in 4Q20, this is still considerable growth given the internet and social media restrictions during the period, and the traditional network churns that usually follow the December peaks.

Network connected devices and terminals

More than 400,000 New devices were connected to the networks in 1Q21. The new growth in gadgets is a mix of smart, feature and basic phones. At the end of 1Q21, the total number of network-connected devices had risen to 31.2 Million.

Consistent with the previous two quarters, Smartphone additions during the quarter outpaced the number of feature and basic phones connected to the network. This is attributed to the continued prevalence of social media and the internet during the extended Covid control protocols across the country.

Over 200,000 smartphones were added within the quarter growing from 7.9 Million smartphones in December 2020 to 8.1 million in March 2021. In addition, network-connected basic phones recovered from an 8% drop in 4Q20 to post a 4% growth in 1Q 21.

At the end of March 2021, the total number of basic phones connected to the networks stood at 17.9 million gadgets.

Device promotions

The market continued with the launch of device credit schemes by Mobile Network Operators. Following the launch of MTNs ‘Pay Mpola Mpola’ device credit scheme introduced in December 2020, Airtel Uganda Ltd launched a similar smartphone credit scheme in partnership with Asante Finance Services group, Mastercard and Samsung. The phones on offer within the scheme include the Samsung AO1, A3 Core and A11.

The payback period may be stretched over three, six, nine and ten months. Repayments for the devices are drawn from the customer mobile money wallet as well as in-store cash repayments.

Pricing And Promotional Campaigns

Mobile Voice Pricing

Underlying non-promotional and out of bundle call rates remained stable through 1Q21, with Airtel and MTN maintaining pre-paid 4 Shs per second charge for both on-net and off-net calls. This is consistent across all time zones.

Mobile Data Pricing

The pricing of retail mobile data services remains bundle-led, with all licensees maintaining capacity bundle offers rather than Kb and speed-based billing offers. Before March 2021, these had definite validity periods and were supplemented with mid and end week special tariff plans.

The mid and end week special offers are further supplemented with behavioural and usage-based offers by the two leading mobile data providers MTN and Airtel, dubbed “My Paka Paka” and “My Pakalast”, respectively.

In a market-first, MTN launched non expiring bundles under its flagship 4G freedom offers at the end of 1Q21, setting the tone for industry-wide review of bundle validity terms.

Smile communications introduced its Data King Bundle of 115 GBs while LycaMobile also maintained its flagship 100 GB and 50 GB bundles.

The tariff plans in the communications sector vary according to the market segments. Comparative price plans may be accessed at the UCC Accredited Price Comparison website at;

The tariff plans in the communications sector varies according to the market segments.

Comparative price plans may be accessed at the UCC Accredited Price Comparison

website at;

Mobile Money Accounts

Following a clean up of MNO mobile money account registers, the number of active mobile money accounts was revised downwards from 22.5 million accounts to 20.3 million accounts at the end of March 2021.

This represents 66% of the 30.5 million registered mobile money accounts by the MNOs. The 66% account registration-activity conversion rate doubles the African average of 30% account activity.

More than 5 million new accounts were registered on a year-on-year comparison between March 2020 and March 2021. This growth was fuelled mainly by significant fee waivers, increased merchant acceptance and limited movements at the height of the pandemic.

Agent Network

Agent access points have grown by 8%, from 235,790 at the end of December 2020 to 254,930 at the end of March 2021. Important to note in this space has been the increased agent interoperability, especially in the CBD. Presently, many mobile money agents have added Bank Agency services to their service portfolio.

Domestic Voice Services

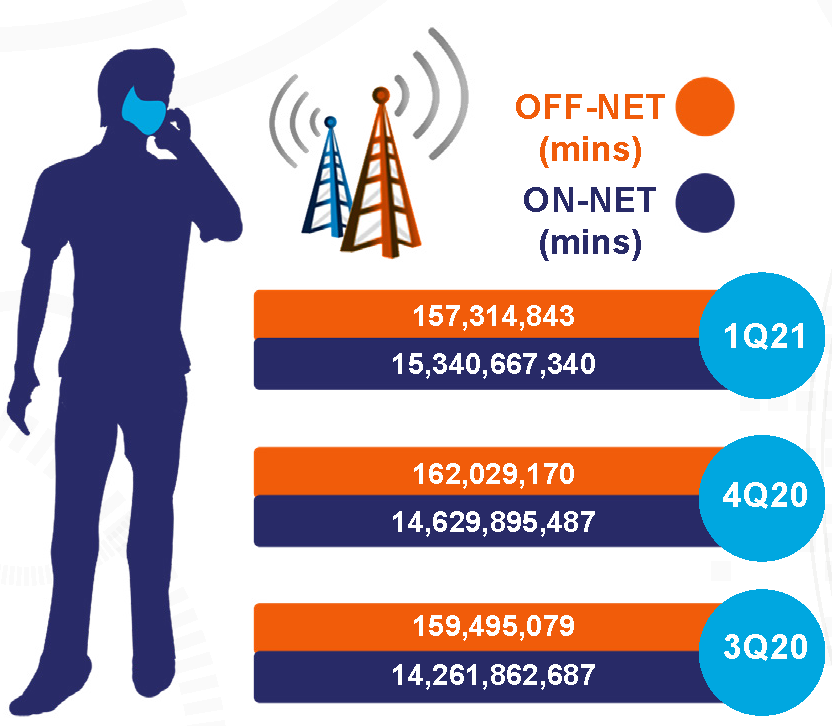

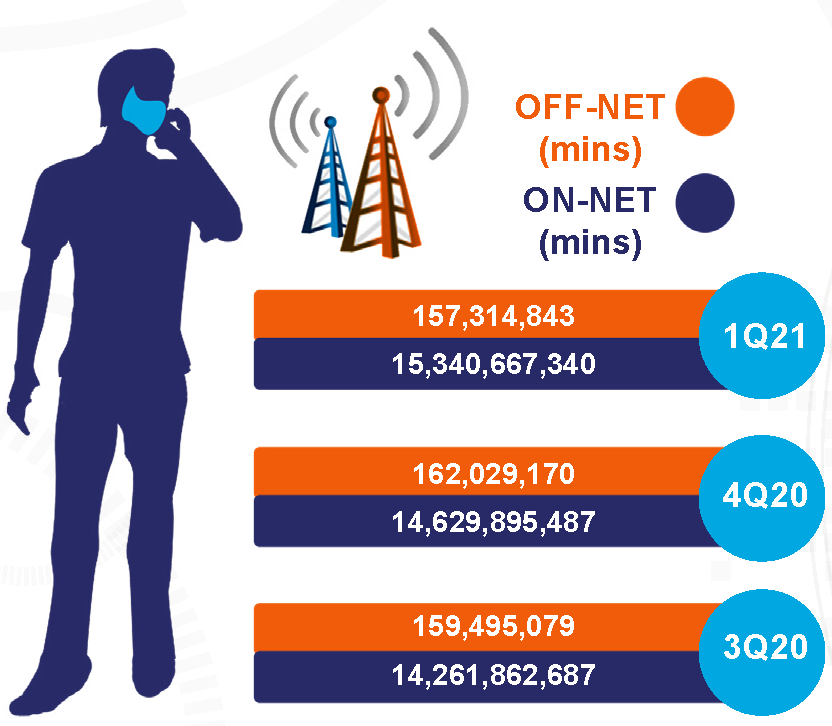

Resulting from the pricing promotional offers and a slight subscription growth highlighted in the preceding segments, the sector recorded a total of 15.5 billion billed minutes, up from 14.8 billion minutes recorded in the quarter ending December 2020.

Subsequently, this resulted in a 5% quarter to quarter aggregate growth in traffic from 3% posted in the preceding quarter. As a result, the market averaged 5.1 billion on net minutes per month during the quarter, with an on-net monthly traffic peak in March of 5.2 billion minutes.

The dominance of on-net traffic is attributed to the pricing differential caused by discounted promotional bundles coupled with spend and usage profiling offers by the telecom operators.

During 1Q21, the market averaged 181 on-net minutes per subscriber per month or approximately 6 minutes per day. This is just about the same as the preceding quarter. The market averaged 52.4 million off-net minutes per month during the quarter, with an off-net traffic peak in January of 54.5 million minutes.

The above translates into an average of 1.86 off-net minutes per month per subscriber during 1Q21.

Broadband Traffic

Broadband usage and consumption during 1Q21 was driven mainly by political campaign messaging and work from home demand. During 1Q21, a total of 58 Billion MBs were downloaded in Uganda. While this is an 18% drop from the record downloads of 4Q20, it represents an almost 20% growth between 1Q20 and 1Q21.

International Voice Traffic

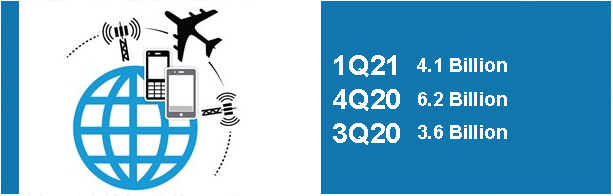

Total international outgoing traffic posted a strong recovery with 49.6 million minutes in 1Q21, a 19% rise from 41.6 million minutes in 4Q20.

This positive gain is attributed mainly to the ‘scientific’ elections during the quarter, which shifted customers into traditional voice services. In addition, there was a 45% rise in traffic. This again provides strong evidence for the impact of OTTs on conventional voice and SMS segments.

As observed in previous quarters, Northern Corridor partner states remain the top destination for international calls with over 70% share of total international traffic.

Unstructured Supplementary Service Data (USSD)

USSD sessions have been growing at an average of 10% between 1Q20 and 1Q21. 1Q21 posted 7.6 Billion USSD sessions in comparison to the 5.3 Billion USSD sessions posted in 1Q20.

The total number of sessions averaged 2.5 billion per month during the quarter. The quarterly peak was realised in March 2021 with a total of 2.7 billion USSD sessions. The growth observed in mobile financial services is positively correlated to the increase in USSD sessions. This is exhibited by an extra 2.2 billion sessions in comparison to 1Q20.

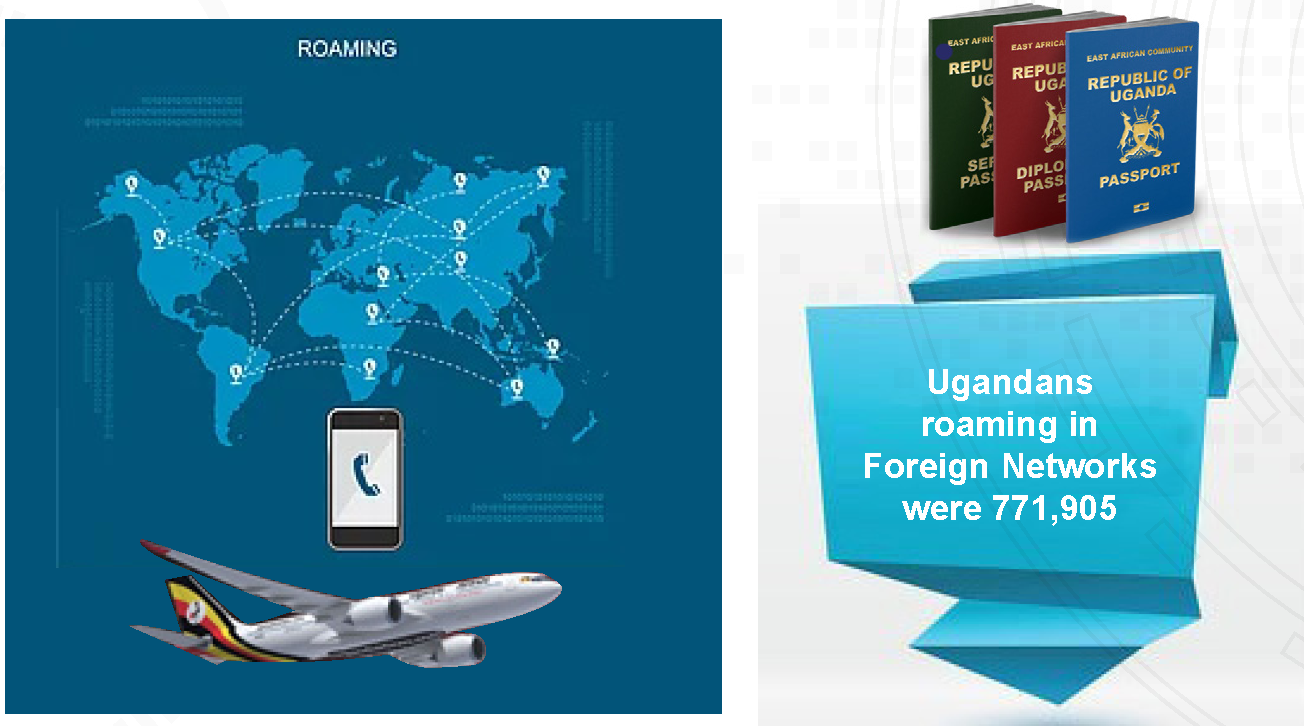

Roaming Service

1Q21 saw a 10% increase in the total number of inbound roamers (Foreigners roaming on Ugandan networks) compared to 1Q20. At the end of March 2021, the number of inbound roamers was 919,382 compared to 838,920 in 1Q20. Of these, 66% are from ONA countries.

Similarly, the number of outbound roamers (Ugandans roaming in Foreign Networks) stood at 771,905, indicating an 11% increase compared to 1Q20.

The industry yet again posted quarterly gross revenues over and above the 1 Trillion mark, with UGX 1.12 Trillion garnered in 1Q21. This reflects a 7% increase in gross revenue compared to the revenue performance of the industry in 1Q20, which stood at UGX 1.05 Trillion.

In terms of Quarter-on-Quarter comparison, industry revenues dropped by UGX 20 Billion from the previous record quarterly performance of UGX 1.14 trillion in 4Q20 to UGX 1.12 Trillion in 1Q21.

International Interconnect Position

Total industry monthly revenues from incoming international traffic have averaged UGX 9.9 billion in 1Q21, increasing almost UGX 600 million compared to the preceding quarter.

Outbound international interconnect settlements have also increased, averaging UGX 6.5 billion per month in 1Q21 compared to UGX 6 billion in 4Q20. This correlates with the volumes of international outgoing voice traffic that increased by 19% between 4Q20 and 1Q21. As a result, during 1Q21, Uganda has posted a positive balance of payments position (BoP) with respect to international traffic settlement, with a net positive of UGX 10 billion.

Order Fulfilment And The Courier Space

Restricted travel movements amidst the slow resumption of business worldwide have continued to provide growth opportunities in the order fulfilment unit of the post and courier industry.

In 1Q21, many last mile order fullment providers like Aramex, Fedex, UPS (Freight in Time) and DHL posted record revenues on account of in-country last-mile delivery services. DHL, in particular, recorded a quarterly turnover of Eur 18,860 Million compared to Eur. 15,464 Million realised in 1Q20. Pan African Operator Jumia, on the other hand, posted Eur. 20.2 million in 1Q21 compared to Eur. 19.1 Million realised in 1Q20.

The operators mentioned above only infer that adopting the latest mobile technologies is playing a significant role in the growth of e-commerce, with local and foreign businesses adapting to new business models to stay afloat.

This has created new opportunities for posts and couriers, encouraging them to evolve services and business models to adapt to new possibilities. As a result, the post and courier sector in Uganda has evolved to a tune of 33 licensees as of March 2021. Over 60% of these operators are Domestic license holders.

These operators use several pickups/drop off centres for the delivery and processing of mail. In the quarter under review, the total number of pickup/drop off centres increased from 483 in 4Q20 to 571 in 1Q21.

Mail Volumes

Incoming and outgoing post and courier traffic posted a positive recovery averaging 72,000 units during January – March 2021, up from an average of 35,000 units in 4Q20. 1Q21, therefore, posted a record positive recovery of 218,000 incoming and outgoing mails, from 148,000 in 4Q20.

The recovery is synonymous with the resurgence of e-commerce platforms such as Amazon, Jumia and the DHL e-africa shop that have enabled last-mile deliveries. This might be explained by the increasing incoming international registered postal and courier items that account for 46% of total mail traffic.

The post and courier segment posted an average of 2.5 billion in 1Q21 and a quarterly total of 7.5 billion. Revenue from domestic mail accounts for only 9% of total revenue. This indicates that international postal and courier items have continued to outgrow traditional mail accounting for 91% of mail traffic revenues through international operators such as FedEx, Aramex and DHL.

{kind=link}